Portfolio Positioning for 2026 and Beyond...

At first glance, the market looks stretched. The S&P 500 is trading more than ten percent above its 52-week moving average, valuations are elevated, and sentiment feels crowded. For many, that’s enough to conclude risk is asymmetrical and the prudent move is to step aside.

But markets don’t move on valuation alone. They move when capital changes its mind about risk. What we’re seeing now isn’t speculative excess — it’s a deliberate repricing of where money believes it can remain productive while avoiding fragility. That distinction matters, because it reframes the entire setup.

Technically, the S&P has pushed into a zone that deserves respect. Price is pressing against a cluster of Fibonacci extension levels drawn from multiple timeframes — a convergence that rarely goes unnoticed. When unrelated technical frameworks point to the same region, markets tend to pause. Not because demand disappears, but because conviction shifts.

These pauses are not failures. They are decision points. Historically, this is where leadership begins to change, even if the index itself continues higher.

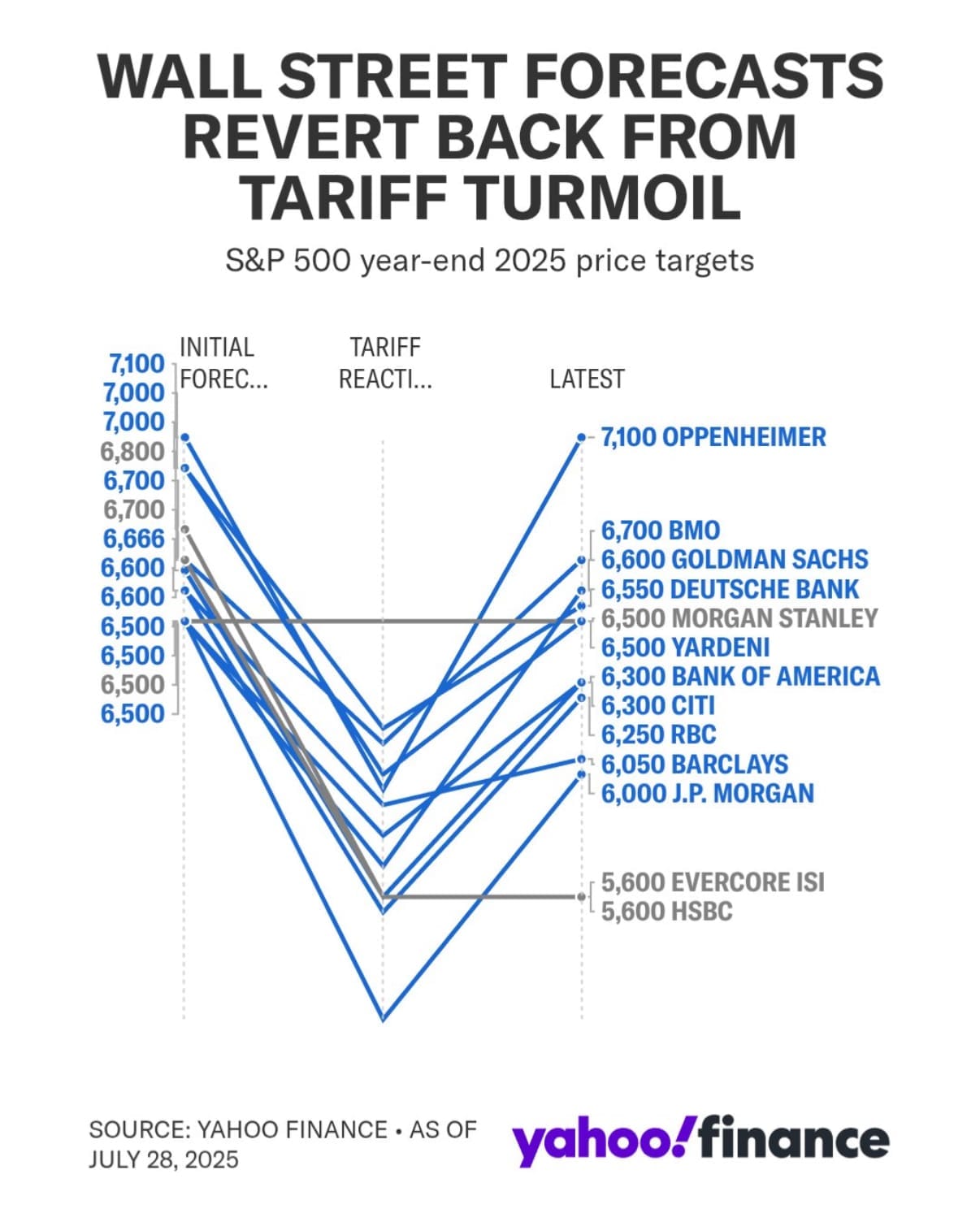

Small Caps & Value outperform the s&P500 over 3-month period. Significant? Small Caps rally amongst falling interest rates, however, really might be haulted by divided FED and haulting more cuts into 2026?

While most attention remains fixated on mega-cap performance, something quieter has been developing beneath the surface. Small-cap and value stocks have begun to outperform the S&P over recent months — not in explosive fashion, but consistently enough to be meaningful.

This isn’t random. Smaller companies are far more sensitive to liquidity expectations than to absolute interest-rate levels. They don’t require aggressive easing — they require clarity. When rate volatility subsides and the path forward becomes more visible, capital that has been hiding starts to edge outward. First cautiously, then with intent.

This is how rotations begin. Not with headlines, but with relative strength.

Since the 2021 highs, large-cap indices have outperformed small caps by a wide margin. That divergence didn’t erase value — it created it.

The early stages of the AI cycle rewarded scale, visibility, and balance-sheet dominance. That phase is well underway. The next phase looks different. Smaller companies don’t need to lead innovation to benefit from it. They need survivability, access to capital, and the ability to adapt.

When liquidity broadens, re-rating happens faster than most expect. That’s where asymmetry lives.

Portfolio Structuring When Risk Is No Longer Binary

There’s a misunderstanding about “low risk” portfolios that needs to be addressed upfront.

Low risk does not mean sitting in cash, waiting for catastrophe, or opting out of markets entirely. It also doesn’t mean outsourcing responsibility to a money market fund and calling that prudence. If that’s your framework, this probably isn’t the right newsletter for you.

Risk is not something you eliminate.

Risk is something you allocate intelligently.

And in the current environment, not participating is itself a form of risk—one that quietly compounds opportunity cost while inflation, currency debasement, and asset repricing do their work in the background.

The Market Is Telling You Where Capital Wants to Live

Strip away the headlines and the noise, and one signal keeps reappearing across asset classes: capital is searching for permanence.

The persistent rise in precious metals, the resilience of equities despite restrictive policy, and the bid under select real assets all point to the same conclusion—this is still a risk-on environment, but not the reckless kind. It’s a discriminating risk-on. Capital is flowing away from promises and toward things that feel structurally scarce, productive, or insulated from policy error.

This isn’t accidental.

For several years now, Ray Dalio has been explicit about what he views as a long-term unwind of fiat confidence—a slow, non-dramatic erosion rather than a sudden collapse. He reiterated this again recently at World Economic Forum, emphasizing that the shift away from traditional fiat systems isn’t ideological—it’s practical. Governments issue too much. Debt grows faster than productivity. Purchasing power erodes quietly.

You don’t need to agree with every part of that thesis to recognize its fingerprints in the market.

When Cultural Signals Confirm Capital Flows

One of the more revealing moments didn’t come from a central banker or a policy speech—it came from culture.

A global livestream personality traveling through Africa casually asked whether a vendor could accept a traditional U.S. payment app. Then he asked if they could accept USDC or USDT. The answer was yes.

That moment mattered—not because of who asked the question, but because of how unremarkable the answer was.

This wasn’t novelty. It was normalization.

What people loosely call “debanking” or “exiting fiat” isn’t a singular event. It’s a behavior shift. A gradual preference for rails that move faster, inflate less, and rely less on intermediaries. Crypto, metals, and even select equities are all absorbing this flow from different angles.

Bonds Aren’t Broken—They’re Obsolete (For Now)

The traditional ballast of conservative portfolios—the bond market—has failed its mandate.

For decades, bonds were supposed to do three things:

- Preserve capital

- Provide yield

- Hedge equity drawdowns

They’re currently doing none of them particularly well.

As rates peaked and growth slowed, bonds failed to offer upside convexity. As inflation lingered, they failed to protect purchasing power. And as equities surged, they became dead weight rather than stabilizers.

Our working theory is that a meaningful portion of liquidity driving gold, silver, and even crypto inflows is coming from ex-bond capital—investors reallocating away from instruments that no longer compensate them for duration risk.

This is especially relevant as money market yields compress. When the “risk-free” return begins to shrink, capital doesn’t sit still—it migrates.

The Quiet Divergence Everyone Missed

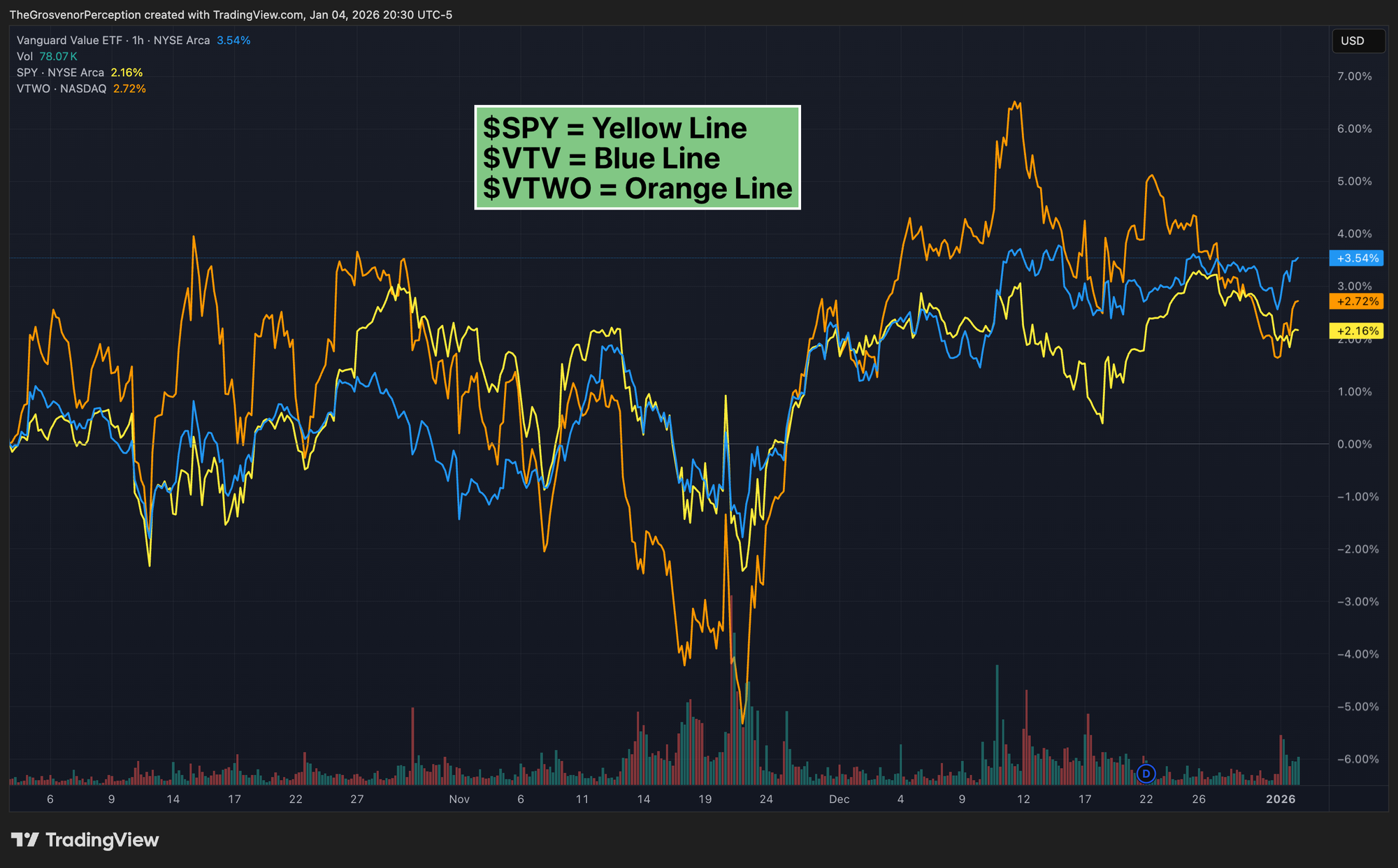

Since the 2021 highs in the Russell 2000, the S&P 500 has outperformed small caps by roughly 30%.

That divergence tells a story.

The AI revolution and passive flows have allowed mega-cap names to dominate index returns and media attention. Meanwhile, a broad swath of small-cap companies have been quietly restructuring, deleveraging, and adapting—without the benefit of narrative tailwinds.

We view that as opportunity, not neglect.

If you’ve been following this newsletter, you’ve already seen how selective exposure to small caps can outperform when sentiment eventually turns. And we continue to see substantial upside into 2026 and 2027 as capital rotates down the market-cap spectrum.

Parabolic moves don’t start with headlines. They start with positioning gaps.

Risk Management Doesn’t Mean Playing Defense Everywhere

That said, concentration risk cuts both ways.

Small caps will not move in a straight line. They never do. Which is why downside protection matters—not through broad hedges that dilute returns, but through complementary positioning.

We favor defensive companies that:

- Generate consistent cash flow

- Pay sustainable dividends

- Operate as leaders within essential industries

Names like Costco, ConocoPhillips, and Chevron fit this profile—not as speculative upside plays, but as stabilizers that allow more aggressive exposure elsewhere without destabilizing the portfolio.

Defense isn’t about fear.

It’s about earning the right to stay invested.

A Low-to-Moderate Risk Allocation That Still Participates

For investors who view the current environment as uncertain—but not apocalyptic—a balanced structure might look something like this:

- 30% Small-Cap Equities

Focused on balance-sheet strength and asymmetric growth potential - 30% Defensive, Dividend-Oriented Leaders

Cash-flow resilient, inflation-aware, sector-dominant - 30% Cash or Cash-Equivalents

Not as a retreat, but as dry powder and volatility optionality - 10% Alternatives

Options or futures strategies designed to express views efficiently rather than chase beta

This is not static. It’s a framework that evolves as volatility, rates, and liquidity conditions change.

And this is where the real differentiation begins.

Because once we move beyond moderate risk tolerance and into full risk-on positioning, the conversation shifts entirely—from preservation to capital velocity, from balance to asymmetry.

That’s where we’ll go next.

For paid subscribers, that’s where we already are.

Disclosure Statement for The Grosvenor Perception

Last Updated: 08/02/25

General Disclaimer

The Grosvenor Perception (“we,” “our,” or “the publication”) is a financial newsletter published by Michael Harbin. All content published in this newsletter, whether online, in email, or through any affiliated platforms, is intended for informational and educational purposes only. None of the information contained herein constitutes investment, financial, legal, or tax advice.

The views expressed in The Grosvenor Perception represent the personal opinions and analysis of the writers and contributors as of the date published and are subject to change at any time without notice. These opinions do not reflect the views of any affiliated institutions, employers, or entities.

No Investment Advice or Recommendations

The Grosvenor Perception is not a registered investment advisor, broker-dealer, or financial planner. We are not licensed under the U.S. Securities and Exchange Commission (SEC), Financial Industry Regulatory Authority (FINRA), or any other regulatory agency in any jurisdiction to provide personalized financial advice or investment recommendations.

Nothing published in this newsletter or on our website should be construed as a solicitation, offer, or recommendation to buy, sell, or hold any security or financial instrument. Subscribers and readers are solely responsible for their own investment decisions and should consult a licensed financial advisor, tax professional, or legal advisor before making any financial or investment decisions.

No Guarantee of Results or Performance

While we strive to provide accurate and up-to-date information, The Grosvenor Perception does not guarantee the accuracy, completeness, timeliness, or reliability of any information contained in our content. Financial markets are inherently uncertain and subject to numerous variables; past performance is not indicative of future results.

We disclaim all liability for any errors, omissions, or inaccuracies in the information presented. We make no representations or warranties—express or implied—regarding the effectiveness or profitability of any strategy, investment, or analysis discussed.

Forward-Looking Statements and Speculative Content

Some content in The Grosvenor Perception may contain forward-looking statements, projections, or speculative commentary, which are inherently uncertain and involve risks. These statements reflect our best judgment and interpretation at the time of publication but may not materialize as anticipated due to factors beyond our control.

Conflicts of Interest and Compensation

Writers and contributors to The Grosvenor Perception may have personal investments in securities or assets mentioned in the publication. Any such positions are not intended as recommendations and may be disclosed at the discretion of the author.

The newsletter may also contain sponsored content or affiliate links for which we may receive compensation. Any such material will be clearly marked in accordance with applicable FTC guidelines.

Copyright and Distribution

All content published in The Grosvenor Perception, including text, images, logos, and branding, is the intellectual property of Michael Harbin and is protected under applicable copyright laws. Unauthorized reproduction, redistribution, or public display of any portion of our content without written permission is strictly prohibited.

Jurisdiction and Legal Compliance

This publication is intended for a U.S.-based audience and is governed by the laws of the State of Florida, without regard to its conflict of laws principles. Access to the content of The Grosvenor Perception may not be legal for individuals in certain jurisdictions. It is the responsibility of the reader to ensure compliance with their local laws and regulations.

Contact Information

If you have questions about this disclosure or wish to contact the publisher of The Grosvenor Perception, please reach out to:

The Grosvenor Perception

admin@grosvenorperception.com

By reading this newsletter or accessing our content, you acknowledge that you have read, understood, and agreed to the terms outlined in this disclosure.

Member discussion