Stock Market Update & Economic Outlook - Issue No. 1

2025 has been a year of dramatic swings thus far across many asset classes. We’ve experienced an historic drawdown and recovery in the equities market, a bond market that is on the brink of collapse, and inflation hedge assets such as Gold and Bitcoin that have outperformed due to the high levels of uncertainty.

The introduction of tariffs from the Trump administration have created enormous amounts of fear for many US companies creating the need to restructure financial outlooks and forward guidance.

The S&P 500 has posted a YTD return of only 6.30% (at the time of writing) with a max drawdown of -18.10%. Tech stocks have underperformed the broader market and experienced a max drawdown of -23.81%. The Mag 7 has contributed to over 50% of the overall market cap recovery since the lows on April 7th. S&P 500 in May had the strongest monthly performance since 1990. Although the market conditions have been very tough through the first half of the year, they have also created an immense amount of opportunity for those ignoring the noise and focusing on the proper perspective.

Where do we go from here? Into the end of 2025.

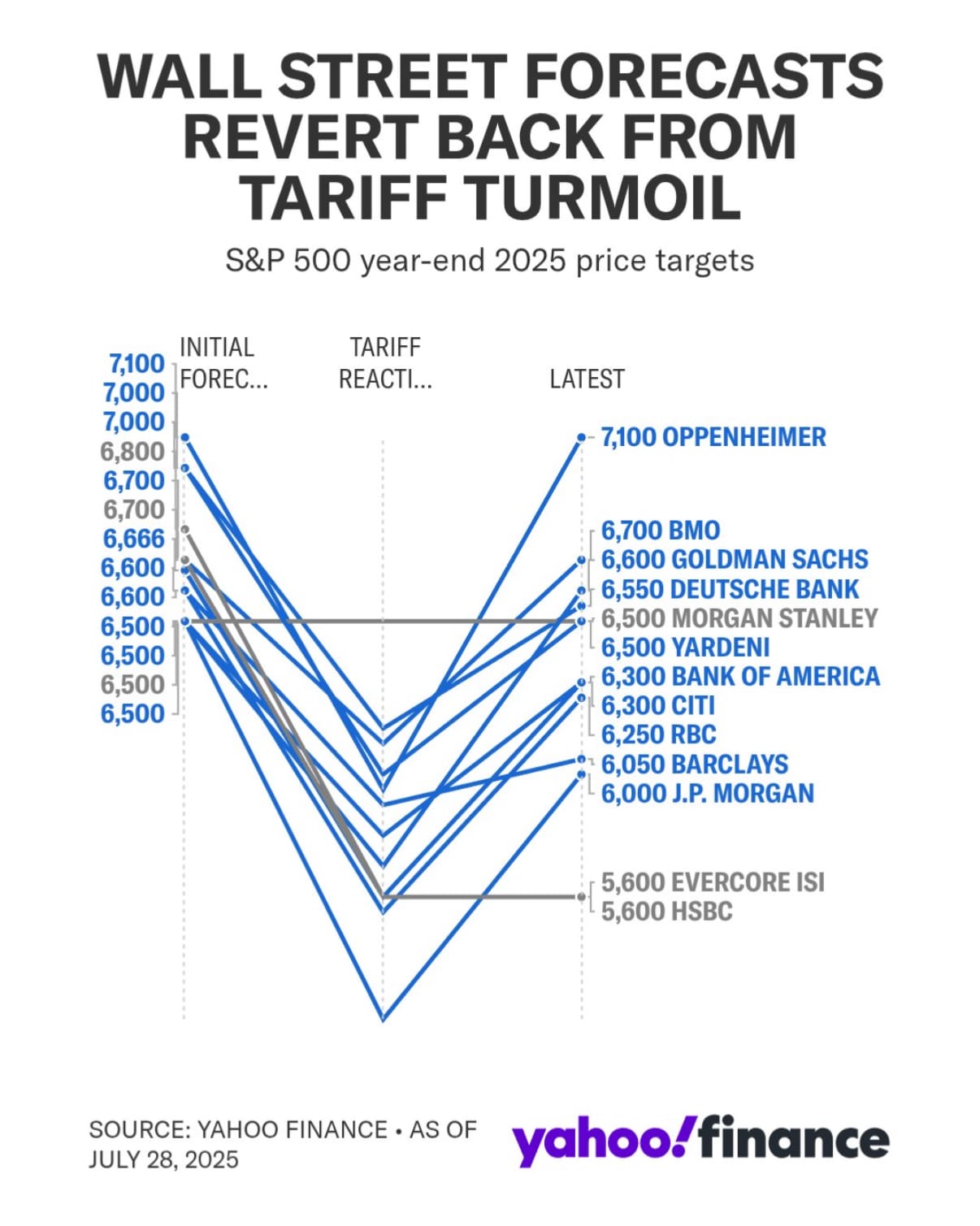

Beginning with the end in mind has been completely missed through the first 5 months of the year. If the S&P 500 were to end at either end of the initial forecast spectrum, the returns will have to range from a minimum of +6.67% to a maximum of +18.33% from current level.

Given the economic contraction we’ve felt, 7100 seems completely out of consideration. The S&P would have to average +2.61% per month for the rest of the year to hit.

Prediction markets have the chance of a recession at 26%, down from 70% a month ago. The biggest worry that we have is the state of the real estate market and what a continued stall in interest rate reductions could do recession odds. Real estate is the heart of our economy and the prolonged squeeze consumers have experienced has expanded household debt and defaults. Along with 50% of Small Caps remaining unprofitable, the overall health of the economy isn’t positioned for a strong Risk-On environment. There seems to be a political bias to the interest rate reduction with the white house pressuring the Fed to cut rates immediately and half of the Fed wanting to keep rates elevated with the anticipation that tariffs will drastically re-ignite inflation.

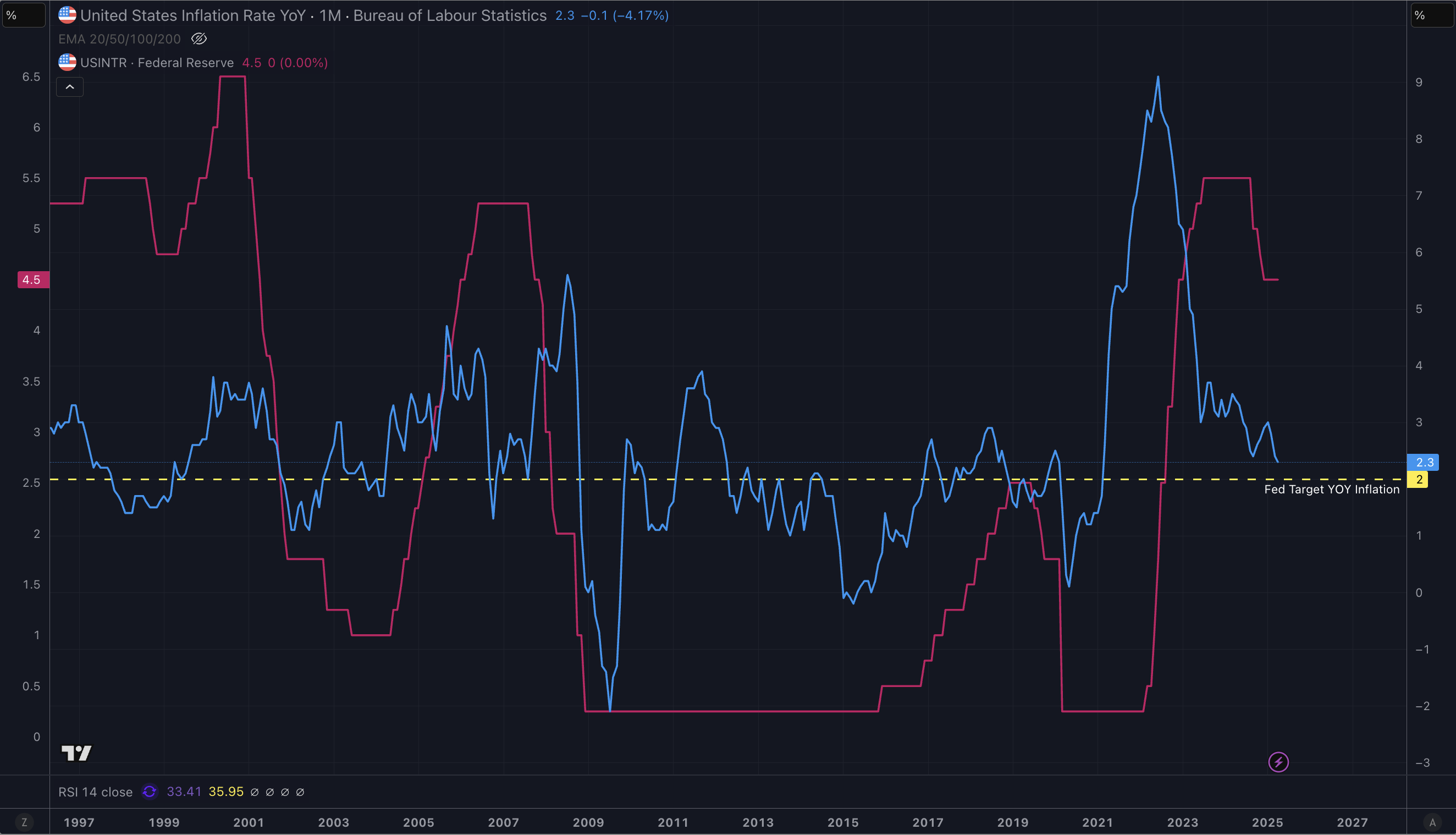

After YOY Inflation peaked in June 2022, the Fed continued to raise rates over the next 13 months. At the end of the rate hike cycle, YOY inflation had already reduced from the high of 9.1% down to 3.2%. As of April, YOY inflation is sitting at 2.3% which is lower than pre-covid lockdown YOY inflation.

The chart above shows YOY inflation rate with the interest rate overlaid. If we evaluate the previous rate cut cycles, a larger cut seems like it should come sooner rather than later. Especially given the diluted value of the US Dollar’s purchasing power over the last decade.

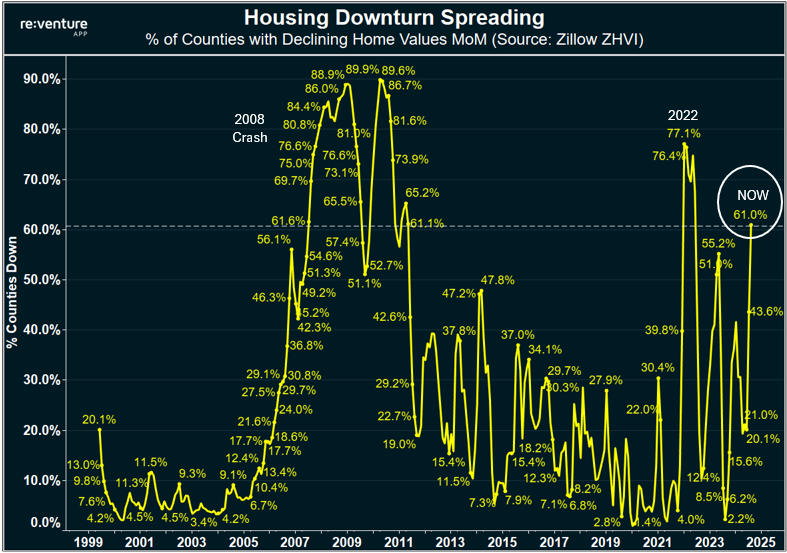

To expand on our concerns around the real estate market and how it might cause drastic impacts across other markets, let's look at a few metrics that show the deteriorating real estate environment. One metric that stands out is the percentage of US counties that are experiencing a decline in home values Month-over-Month.

When compared to the last cycles of the same decline, we can see that the drop in fed funds rate post-covid led to the extreme YOY hike in inflation which led to housing prices to drastically decline MOM. The other similar MOM decline in value was during the great recession of 07’ & o8’ in which the real estate market was destroyed. Take a look at the chart below:

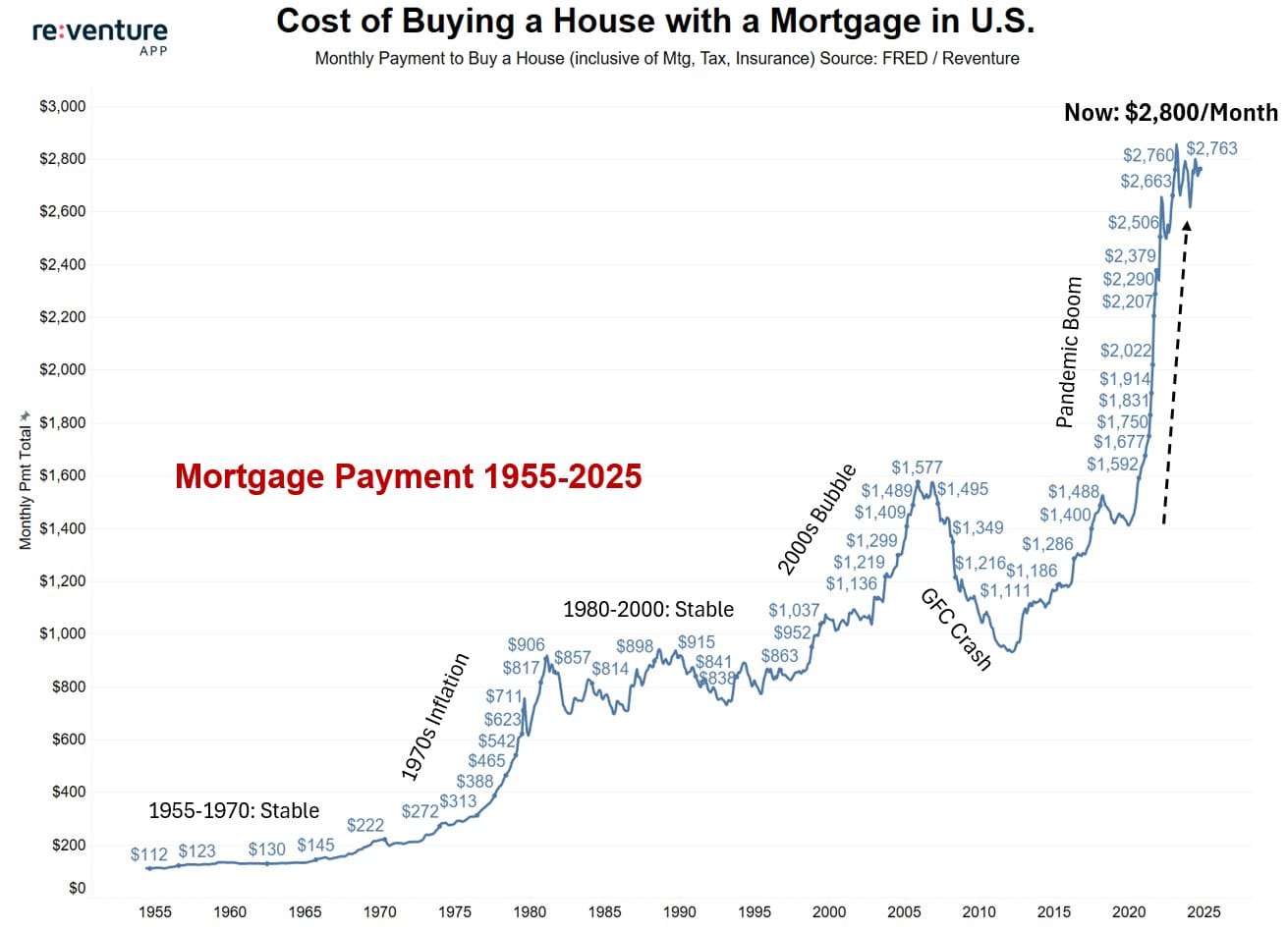

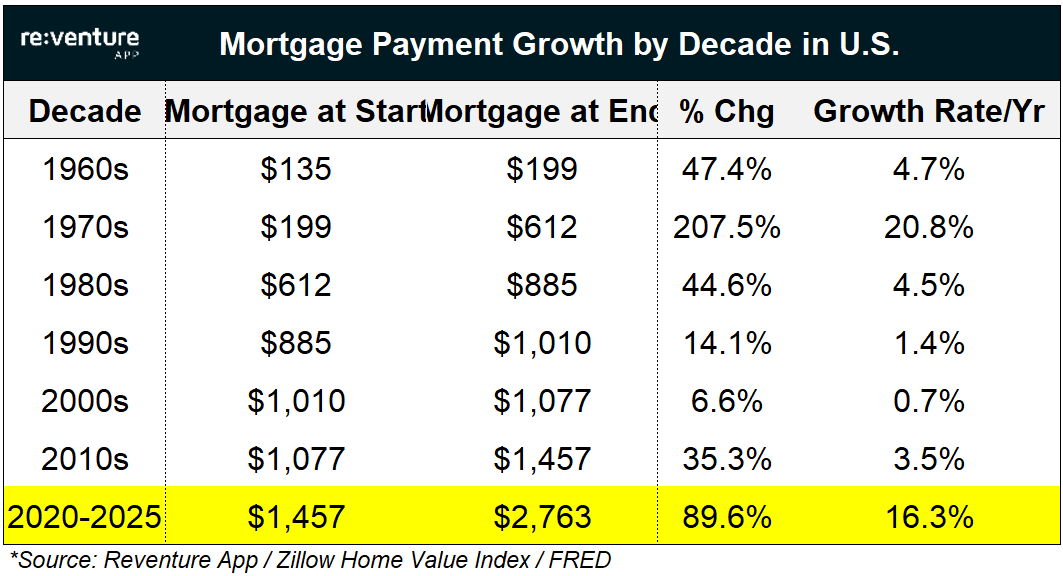

When we take the diluted value of the US dollar into perspective we can see that it has created an almost unaffordable mortgage environment. From 2020 to 2025 mortgages have almost doubled, increasing by 89%. From a historical standpoint, this type of home cost can be sustained and needs to level-out.

All of this also echoes the importance of compounding investment growth. Especially if wage growth is growing at a steady pace. The 2020 to 2025 mortgage increase equates to a YOY growth rate of 16.3%. Compared to the average annual S&P 500 return of 10.52% the impact of mortgage rate growth has obliterated the average American's ability to afford living within comfortable means. This has removed the ability to save and continue putting money aside for investment portfolios.

If you aren’t able to keep up with the rising cost-of-living on top of the steady rise of inflation, as time goes on your ability to provide for the same level of living will eventually turn negative. On a grand scale, this would lead the majority of Americans to over leverage with debt and potentially lead to a debt crisis.

We want to empower our subscribers to not only keep pace with the rising cost of living, but create the opportunity to outperform the S&P 500 and also outpace the external rising cost that is out of our control.

US Conflicts and Concerns

The internal political climate of the United States continues to intensify, with mounting activism on both ends of the ideological spectrum. This polarization appears to be advancing steadily—like a slow-moving escalator—with each passing month. In the opening six months of President Trump’s second term, the administration has enacted several aggressive policy shifts, sparking widespread protests over a number of contentious issues.

Among the most pressing concerns is the escalating conflict in the Middle East. In our view, the war between Israel and Iran has the potential to significantly destabilize global geopolitics. Beyond regional implications, we believe this conflict could act as a flashpoint that further deepens the divide between Western allies and the BRICS nations, particularly China and Russia. These developments are not occurring in a vacuum—they are unfolding against the backdrop of a rapidly evolving global trade environment.

One of the most consequential policy shifts initiated by the Trump administration is the implementation of sweeping tariffs. This new protectionist posture represents uncharted territory—not only for the United States but also for the global economy, as affected nations are now responding with reciprocal measures. While critics of the administration have forecasted these tariffs as a harbinger of surging inflation, we maintain a different perspective.

In our assessment, these tariffs should be viewed as a long-term strategic maneuver. Rather than triggering immediate inflationary pressures, we believe they represent a calculated effort to address structural imbalances—namely, the expanding federal deficit and the unchecked growth of the money supply. If effective, this approach could initiate a mild deflationary trend that would support the strengthening of the U.S. dollar and, in turn, improve the purchasing power of American consumers.

However, this strategy is not without risk. The most existential economic threat facing the United States remains the potential loss of the U.S. dollar’s status as the global reserve currency. Should the dollar falter, the Chinese yuan—backed by the world’s second-largest economy—would be the most likely successor. While it may be tempting to assume that economic pragmatism will foster cooperation between China and the United States, the geopolitical incentives suggest otherwise. It is not in Beijing’s strategic interest to enable policies that enhance U.S. economic dominance, particularly in light of escalating tariff pressures.

China’s long-standing campaign to influence U.S. policy and weaken the ideological foundations of Western liberal democracy is no longer covert. Through state-directed efforts, the Chinese Communist Party (CCP) continues to exploit digital platforms, mainstream media, and gray-zone operations that resemble the very covert tactics pioneered by Western intelligence agencies such as the CIA during the Cold War era.

All of this geopolitical tension and economic realignment brings us to a critical investment thesis—one that we believe holds significant promise both in the near term and over the next decade.

As U.S.-China trade tensions escalate and global supply chains fracture along political lines, we are placing a heightened focus on rare earth minerals—strategic resources vital to the technologies that will define the next era of global competition. These materials are indispensable to the production of advanced semiconductors, batteries, military hardware, and most notably, the infrastructure supporting artificial intelligence.

The exponential growth of AI-related technologies, particularly in the development of hyper scale data centers and enterprise machine learning applications, has clarified where capital and innovation are flowing. Demand for compute power is surging, and the materials that underpin this revolution—rare earths, high-performance chips, energy-efficient cooling systems—are rapidly becoming the new oil.

We see this convergence of geopolitical risk and technological acceleration as a prime window to allocate risk. Our conviction is rooted in both the macro-level strategic realignment of global power structures and the micro-level supply-demand dynamics of emerging technologies.

Rare Earth Minerals

Magnets, particularly rare-earth magnets, play a crucial and often under appreciated role in the physical infrastructure behind high-performance computing (HPC) and artificial intelligence (AI).

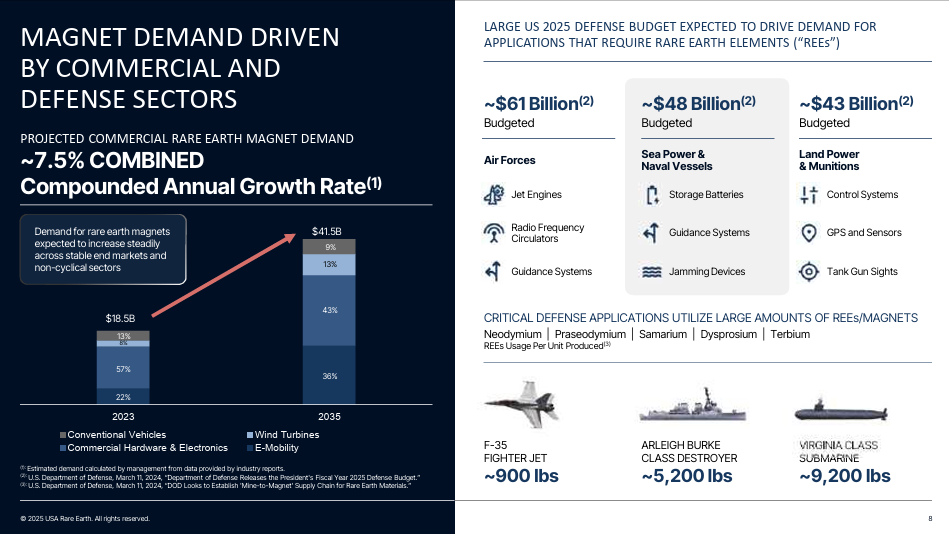

- Global permanent magnet market: $23.4B (2024)

- Projected growth rate: 7.5% CAGR, reaching $36B+ by 2030

- Magnets for AI-related infrastructure (est.): Account for ~15–20% of global high-performance magnet demand in 2024

Their contribution spans from powering electric components to enabling the motion systems of advanced cooling solutions and robotic automation systems in data centers. Let’s break down their value, role in AI infrastructure, key metrics, and supply chain dynamics.

AI hardware, especially GPUs, needs constant innovation in thermal management, power efficiency, and electromechanical support systems—all of which use magnets.

- NVIDIA H100/A100 Cooling Fans - Each uses 2–3 brushless DC motors, each requiring high-strength rare-earth magnets

- Server Power Supply Units (PSUs) - Use magnetic cores to manage power conversion with minimal loss

- Actuators in AI robotics - High-torque, compact, magnet-powered motors for fine control

*A single hyper scale data center may use over 100,000 fans and motors, each using magnets.

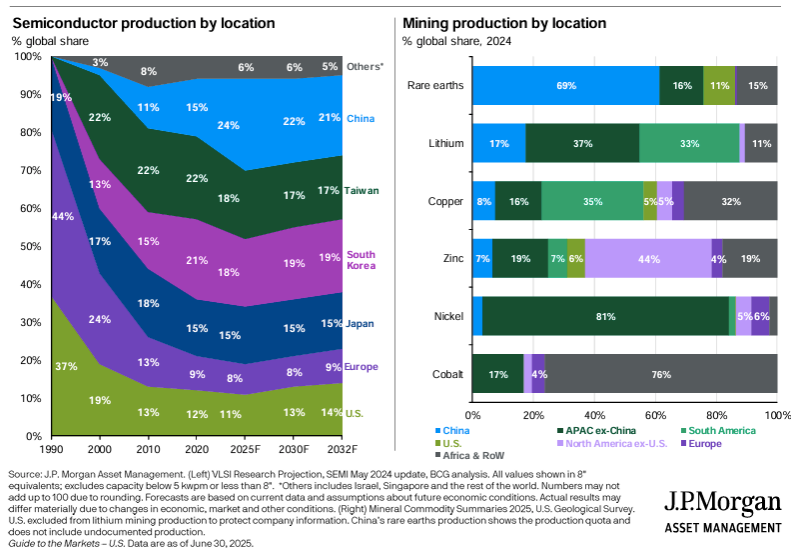

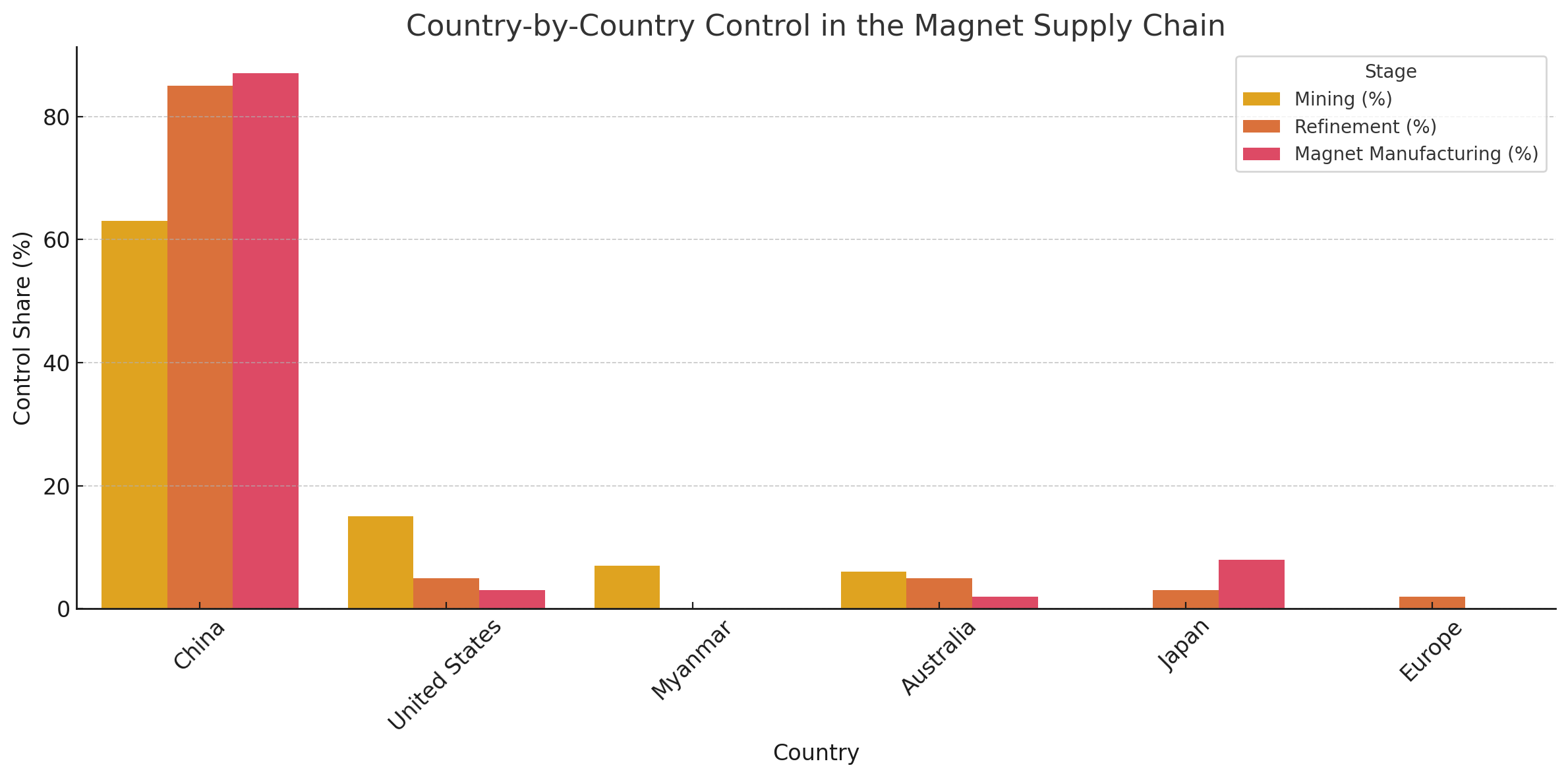

China controls over 85% of magnet-grade rare-earth separation and processing. U.S. firms like MP Materials (Mountain Pass, CA) extract neodymium but still send material to China for processing.

- China 87% - of global sintered NdFeB magnet production

- Japan 8% - (high-tech applications)

- U.S. & Europe - <5%, mostly for defense contracts

Take a look at this plot showing the vast imbalance in the global magnet supply chain.

AI hardware is geopolitically exposed to rare earth magnet supply chains. The U.S. is actively trying to onshore magnet production (e.g., Lynas, MP Materials downstream projects). Without magnets, there is no efficient cooling, no power management, and no motion systems for AI hardware. Magnets directly enable high-density GPU farms that power LLMs, autonomous systems, and inference engines. They are non-substitutable for many precision AI applications due to their magnetic strength-to-weight ratio. The future of AI at scale will increasingly hinge on a stable and secure magnet supply chain.

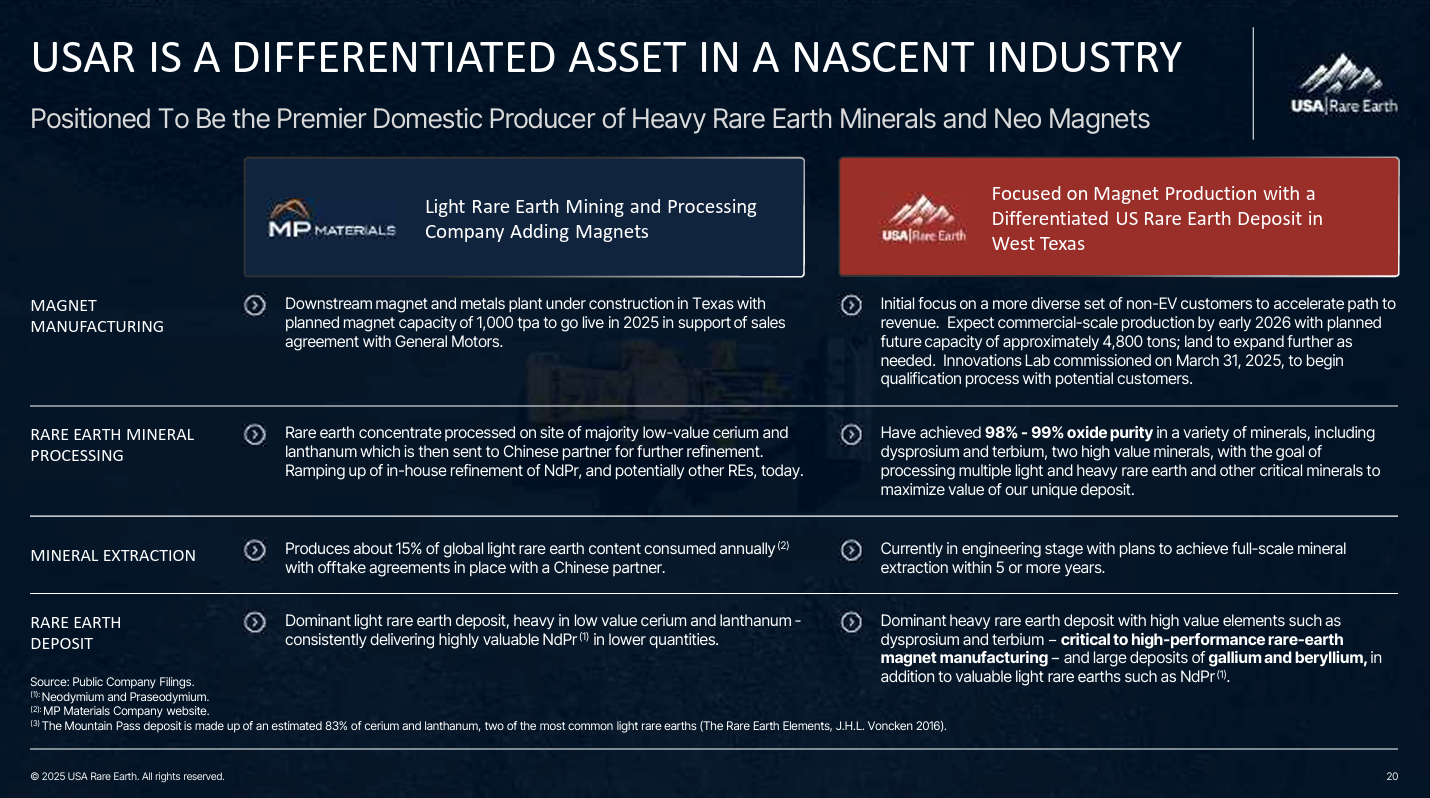

$USAR - USA Rare Earth, Inc.

https://www.usare.com/

USA Rare Earth, Inc. is a domestic supplier of rare earth magnets and heavy rare earth elements. It is developing a vertically integrated, domestic supply chain for rare earth element magnet production, with a facility in Stillwater, Oklahoma, and mining rights to the Round Top heavy rare earth and critical minerals deposit in West Texas. The company was founded in May 2019 and is headquartered in Stillwater, OK. - (Tradingview.com)

Latest SEC filings indicate the company is registering a fixed number of 115,748,969 shares for a share offering under its S‑1 registration and 140,665,609 shares via a secondary offering, plus 6 million warrants, at intervals over time as needed.

Registering the shares legally enables the company to sell them in a public offering or distribute them as planned under the S‑1 registration. This is a key step in raising capital or onboarding new investors. The number is significantly larger than a typical employee incentive registration; it's clearly aimed at a public or large-scale financing, not just internal awards.

The news of the $MP (MP Materials) deal of $400 million of preferred stock purchased from The Defense Department and $APPL (Apple) with a new commitment of $500 million with MP Materials we see a massive opportunity for potential upside in the price of the stock. MPs current market cap is $11.28B and $USAR is currently at $1.34B, 1/8th of the size.

The major difference between $USAR and $MP is that US Rare Earth is pre-revenue and has a lot of progress to make to get their facilities fully operational. Why we don’t foresee this as a major hurdle has to do with the hyper scaling that we are seeing in the AI data center production sector. This has especially been reiterated by all the MAG 7 tech giants as a major reinvestment allocation, now and into the near future, from the recent Q2 earnings statements.

The case use for the products that $USAR intends to produce has only continued to increase as each month passes. These past quarterly earnings reports have indicated that big tech plans on spending hundreds of billions of dollars to develop more and more data centers and the development of key components that are integral to the scaling of both hardware and software.

Our positions in $USAR have long-term (12-24months) price targets between the range of $29 to $40 per share. From current levels this would represent a +200% to +285% return. We believe that the tensions with China have reached a near-favorable situation with an increasing chance that those relations, particularly surrounding the supply chain of rare earth minerals, will worsen as trade tensions and tariffs mature.

The investment deals made by the Trump administration with foreign tech companies to commit hundreds of millions back into the US will only further accelerate the demand for neo-magnet components amongst all the AI competition.

The way we see this setup playing out is a function of energy demand. $USAR has gotten very little public attention even following the recent rally of $MP. As large trends start to form or in this case, start to gain a vast momentum, the inflow of energy will be unstoppable for a given timeframe. The trend that is gaining the most is the development of AI data centers and quantum which will create hyper elevated levels of demand. The more energy the trend accumulates, the more acceleration will take place.

While it’s safe to assume that the AI giants such as NVIDIA, META, AMAZON, etc. will continue to grow in this environment without much resistance, we don’t see the same return profile for the same timeframe.

Ideal long-term price action will be a trend development within the blue parallel channel on the chart above. If the mean of the channel is maintained throughout our timeline, the initial long-term price target at $29 per share will be achieved.

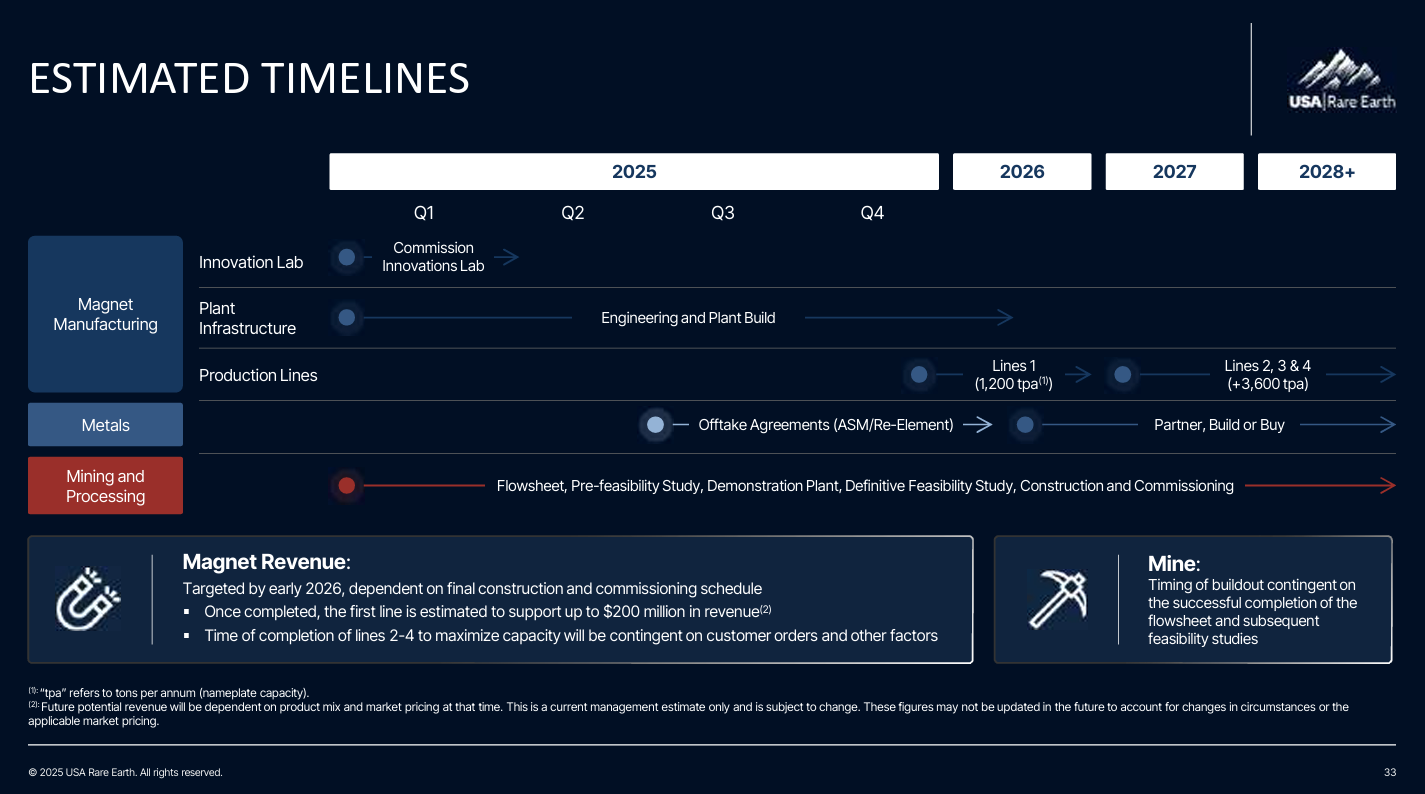

Per their website, $USAR states: “We are building a sintered neo magnet manufacturing facility in Stillwater, OK which is currently planned to go commercial in the first half of 2026. At full capacity, this facility will be able to produce nearly 5,000 metric tons, or hundreds of millions of magnets, annually. We will serve a variety of fast-growing industries, such as defense, robotics, electric vehicles, wind power, appliances, cordless tools and even computing and semiconductors.”

The timeline for our position aligns with the major developments that the company has underway regarding the construction of the neo magnet manufacturing facility in Stillwater, OK. Initial production reports once operational will determine whether or not adjustments will be made to the overall positions we hold as well as industry demand.

For full investor presentation by $USAR visit here - https://cdn.prod.website-files.com/6778240fbac05d2a404af1c0/6824f2dd68cf210cb895383d_April%20Investor%20Deck.pdf

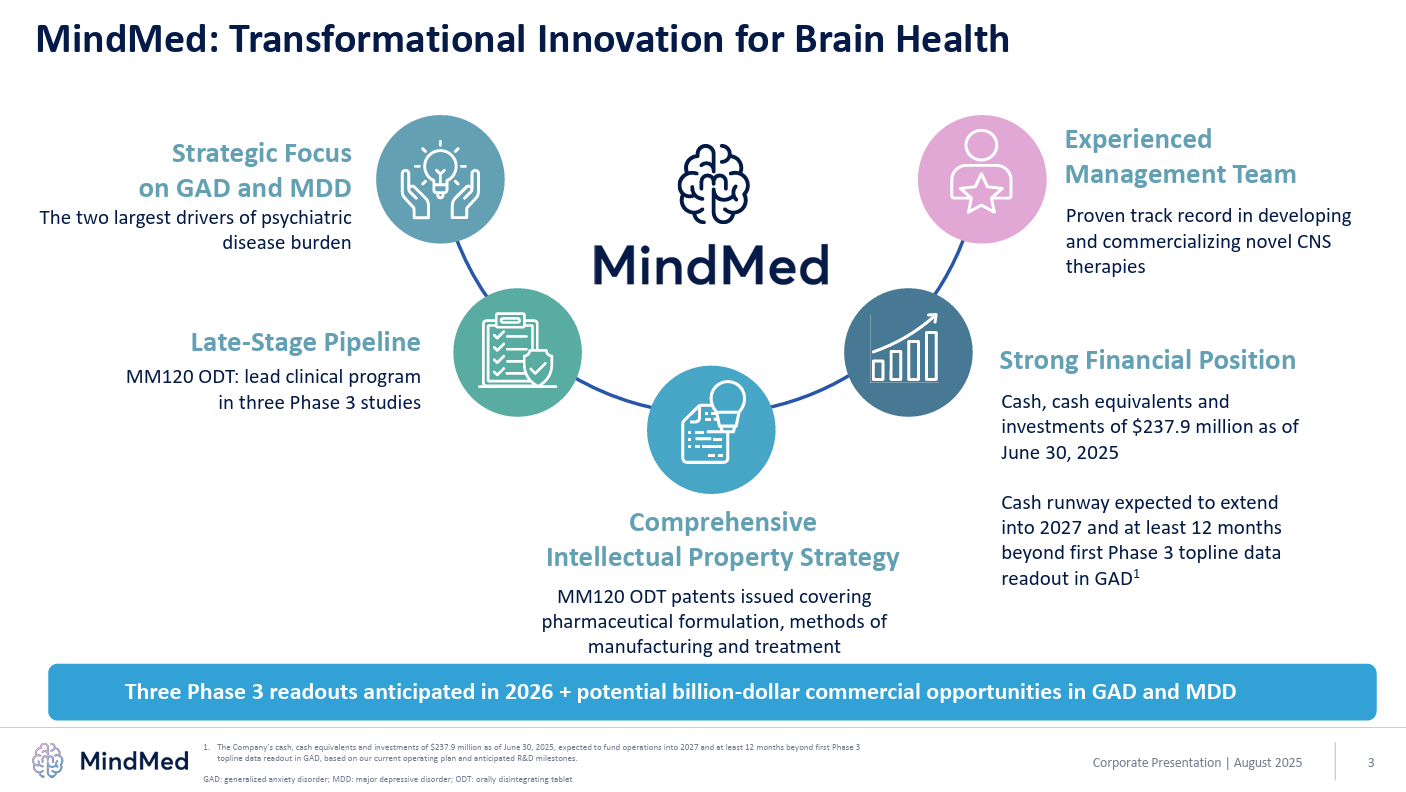

$MNMD - Mind Medicine Inc.

Mind Medicine (MindMed), Inc. operates as a clinical stage biopharmaceutical company, which engages in developing novel product candidates to treat brain health disorders. The company was founded by Stephen L. Hurst, Scott M. Freeman, Leonard Latchman and Jamon Alexander Rahn on July 26, 2010 and is headquartered in New York, NY. - (Tradingview.com)

The Accelerating Mental Health Crisis and the Case for MNMD

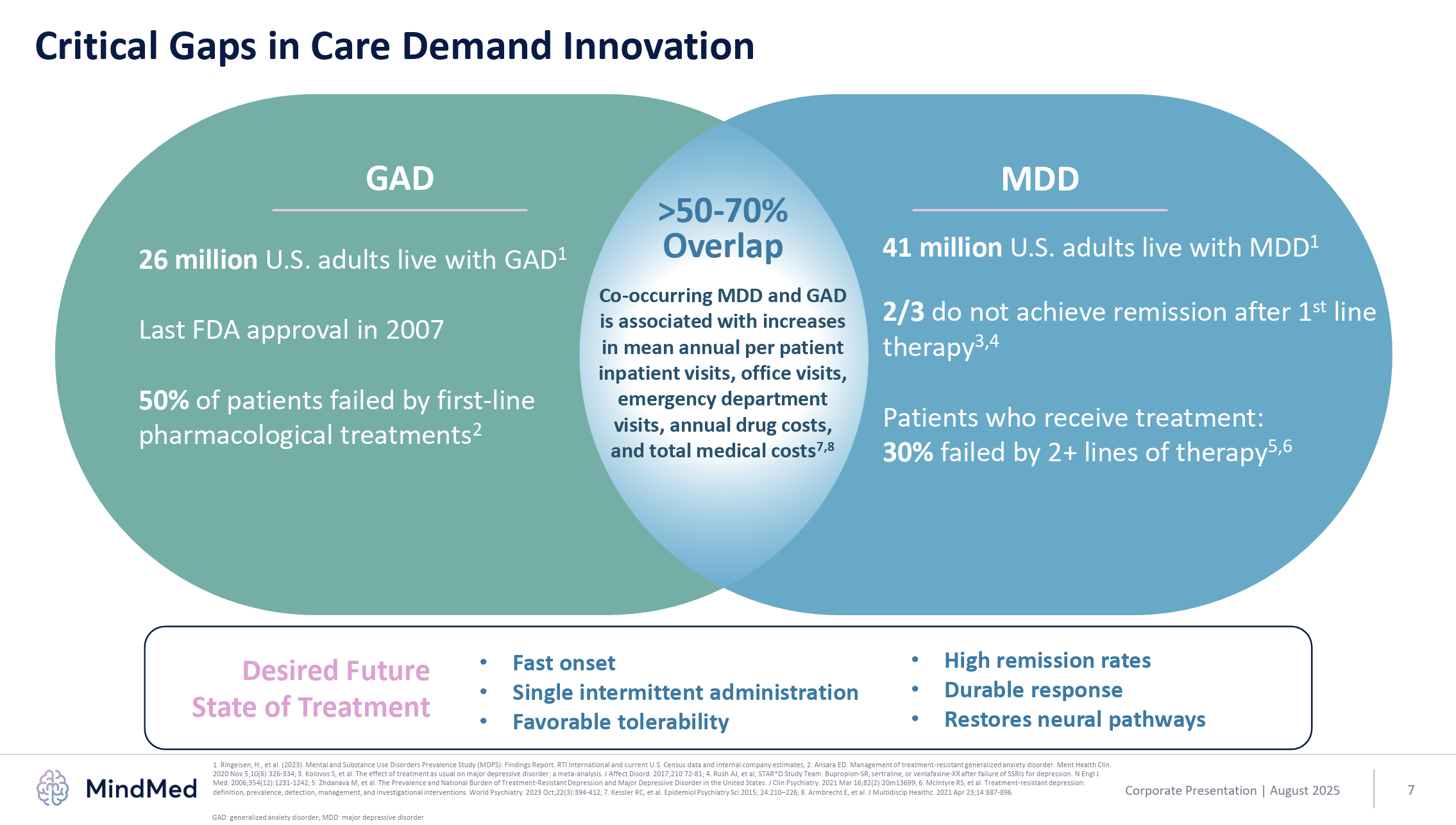

One of the most urgent public health challenges facing the United States today is the accelerating mental health crisis. This is not hyperbole—it’s a visible and measurable trend. On any given week, major media outlets report yet another incident where mental instability has driven someone to an extreme, often violent, outcome. Tragically, one of the most frequent manifestations is gun violence—whether it’s a school shooting, a high-profile attack like the recent shooting of a CEO on a New York City street, or another public incident where lives are lost. Over time, these tragedies have become so common that a level of public desensitization has set in, masking the severity of the underlying crisis.

But mental illness does not need to reach these catastrophic extremes to be profoundly damaging. Millions of Americans quietly battle mental health disorders every day, enduring conditions that erode their quality of life. Among the most prevalent are Generalized Anxiety Disorder (GAD) and Major Depressive Disorder (MDD). These conditions, if left untreated or poorly managed, can evolve into more severe mental illnesses, bringing greater personal and societal risk.

The demand for effective treatment far exceeds the current capacity of the healthcare system. Many patients cycle through multiple pharmaceutical regimens and therapeutic modalities before finding partial relief—if they find it at all. This treatment “trial-and-error loop” results in years of unnecessary suffering, high dropout rates, and economic strain on both individuals and the healthcare infrastructure.

This is where our conviction in MindMed ($MNMD) comes into play. The company’s product candidates—rooted in emerging psychedelic-assisted therapy research—have demonstrated not only the potential for significant clinical efficacy in early and mid-stage trials, but also a lower failure rate compared to traditional pharmaceutical approaches. In other words, these therapies may not just work initially—they may sustain results and reduce the long, costly cycles of ineffective treatment that plague so many patients today.

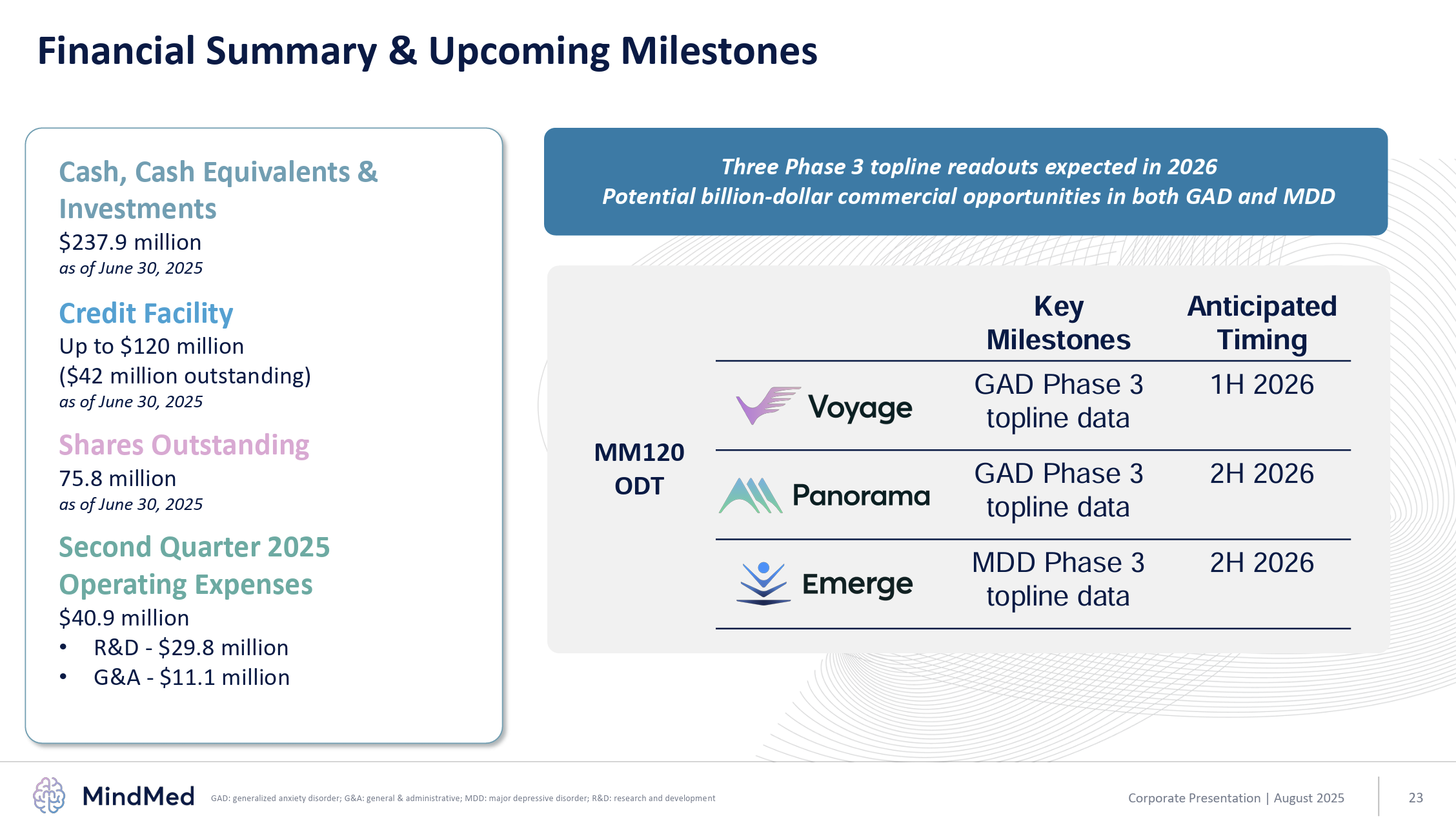

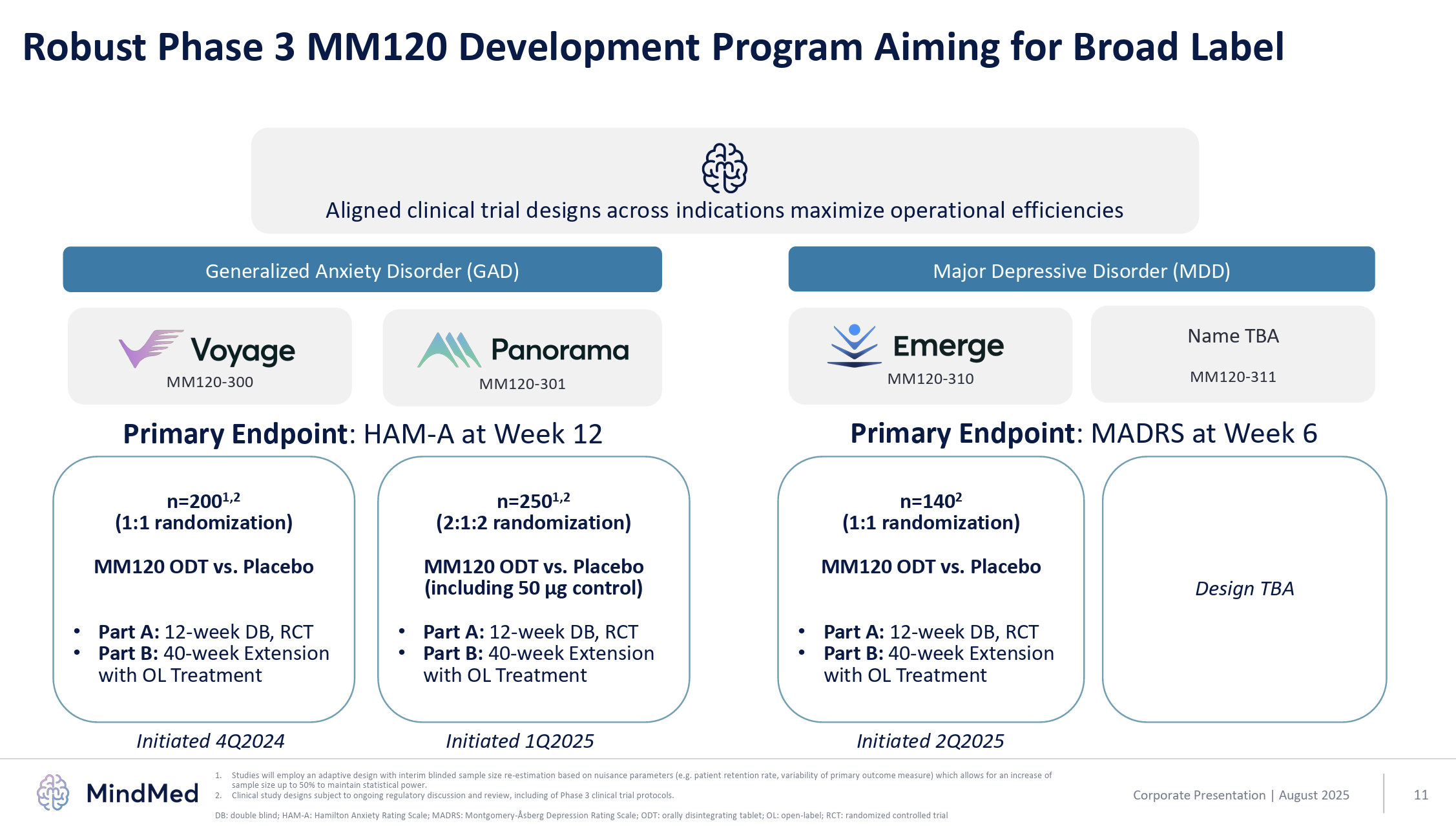

Clinical trial data has reinforced our confidence. Phase 3 trials are currently underway, with results expected throughout 2026. Importantly, these milestones align with a unique political moment: the early tenure of a new pro-health U.S. administration that has already begun to reshape regulatory and public health priorities.

Policy Tailwinds: The “Make America Healthy Again” Agenda

Robert F. Kennedy Jr., confirmed as Secretary of Health and Human Services (HHS) on February 13, 2025, has become the chief architect of President Trump’s “Make America Healthy Again” (MAHA) initiative. This sweeping policy shift aims to move U.S. healthcare away from reactive “sick-care” toward a prevention-first model.

In practice, the MAHA agenda targets ultra-processed foods, harmful additives, environmental exposures, and broken incentive structures, while simultaneously downsizing and restructuring HHS. It also touches politically sensitive areas—altering vaccine policies, increasing public access to federal health data, and rejecting certain international health governance rules.

Key actions to date include:

- HHS Restructuring: In March 2025, Kennedy led a department-wide overhaul, cutting roughly 20,000 jobs, consolidating agencies, and creating the Administration for a Healthy America—a new division focused on preventive health.

- Food Policy Reforms: Initiatives to define and regulate “ultra-processed foods,” close the “Generally Recognized as Safe” (GRAS) loophole for additives, ban certain artificial dyes, and approve state-level bans on soda and candy purchases with SNAP benefits.

- Pharmaceutical and Medical Oversight: Fast-tracking FDA approvals for U.S.-based drug manufacturing, mandating opioid label changes, and overhauling the CDC’s vaccine advisory panel.

- International and Data Policy: Rejecting WHO pandemic treaty amendments, ending certain hospital vaccine-reporting incentives, and expanding public access to health data under the “radical transparency” mandate.

These reforms have the potential to clear decades of regulatory red tape, creating an environment in which novel therapies—especially those that can be shown to deliver durable, preventive benefits—can gain approval and adoption more quickly.

Why Psychedelics Matter—A Historical Lens

Psychedelics, particularly LSD, have a complicated history in the United States. Their therapeutic potential was recognized as early as the 1940s, with early research—much of it during and after World War II—suggesting possible benefits for depression, anxiety, and even dementia.

However, after the war, U.S. intelligence agencies seized on LSD for darker purposes. Through the CIA’s MKUltra program and its subprojects (such as “Operation Midnight Climax”), the drug was tested—often without consent—for interrogation, mind control, and psychological experimentation.

This clandestine misuse, combined with the 1960s counterculture’s embrace of LSD as a consciousness-expanding tool (led by figures like Timothy Leary), fueled a political backlash. By 1966, LSD was criminalized, and legitimate research into its therapeutic benefits was all but extinguished for decades.

Only recently—through what’s now called the “psychedelic renaissance”—has serious clinical research resumed. Modern studies are more rigorous, better regulated, and focused on safety as well as efficacy. The early data has been compelling enough to suggest that psychedelics, used in controlled therapeutic contexts, could help treat conditions that have resisted conventional pharmaceuticals for decades.

Investment Outlook

The convergence of three forces:

- A worsening mental health crisis,

- The promise of psychedelic-assisted therapy as a disruptive treatment model, and

- A political environment actively dismantling regulatory barriers.

…creates a unique investment window for companies like MindMed. If Phase 3 data confirms the efficacy and safety already seen in earlier trials, $MNMD could not only gain approval but also enter the market in an era of accelerated adoption and supportive policy.

For long-term investors, this may represent one of the most asymmetric opportunities in the current healthcare innovation landscape.

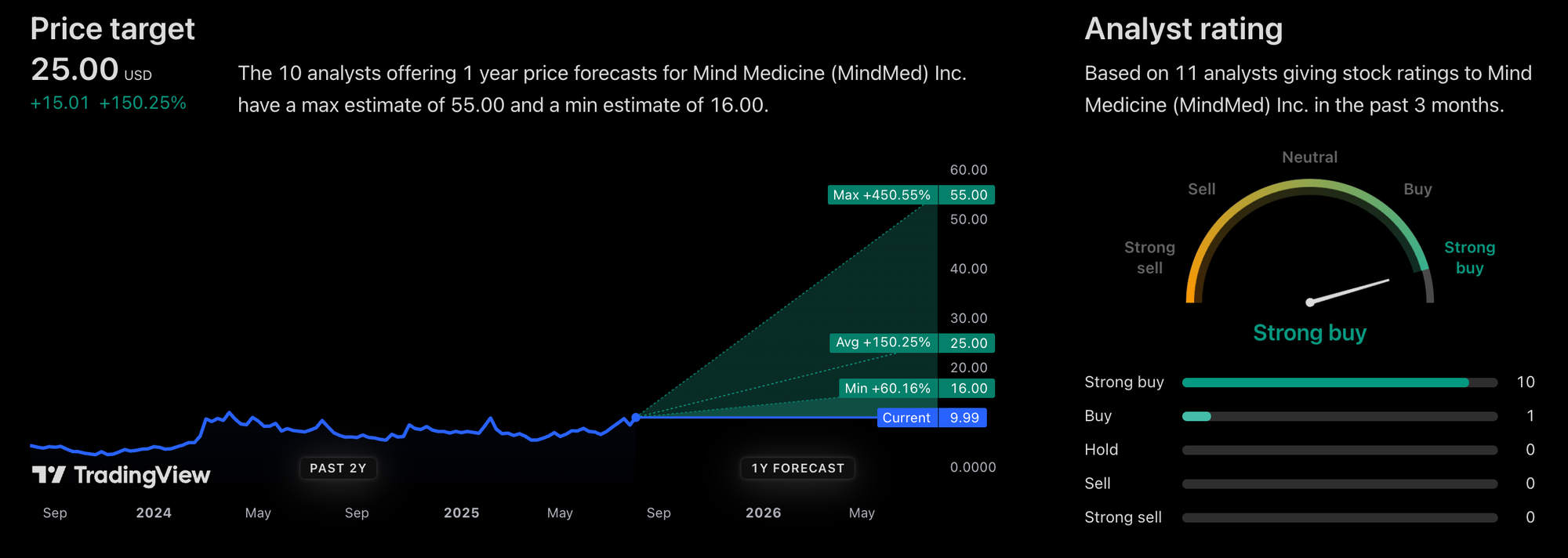

Analysts covering MindMed (NASDAQ: MNMD) project a 12-month target of $25, suggesting a potential upside of approximately +150% from the current trading range—though estimates range widely between $16 and $55. The consensus among 11 analysts remains firmly at “Strong Buy.”

For full investor presentation by $MNMD visit here - https://ir.mindmed.co/news-events/presentations

What else do we see?

Going into the later half of the year, we are taking a more selective approach to any new positions. We see the overall markets having a volatile consolidation within a range of +/- 7% from current levels for the next few months. End-of year projections for us aren’t as important at this point in the year as much as the price action will be going forward.

Our outlook for Q1 2026 will be heavily weighed by how the year end actually closes for the overall markets. One of the continued major factors that has had an impact on asset prices is the unknown path of interest rates.

The projections for a September rate cut currently have a 25bps cut at 80% likelihood. With the recent revisions to the jobs data, we anticipate a potential broadening of unfavorable labor data which could influence the possibility of a cut >25bps.

The response of DXY (US Dollar) to the recent tariff deadline of Aug 1st has signaled the likelihood of continued inflows into inflation hedge assets such as Gold and Bitcoin. Continued macro trend of DXY weakness will greatly influence our position hedges into those markets either through options strategies and spot ETF holdings.

DXY is facing a multi-decade trendline breakdown. A breakdown of this trend would likely create a strong case for keeping interest rates higher for even longer. Any reduction in rates would only accelerate the devaluing of DXY.

Another negative side effect of a declining dollar is the negative impact it will have on the bond market which would also keep rates elevated to encourage the purchasing of US bonds to investors seeking higher rates.

We will continue to learn towards hedge assets such as Bitcoin and Gold. Due to the nature of Bitcoin and it's historically volatile price action, we will capture even greater opportunity with the use of options contracts on proxies such as $IBIT. Gold will remain as a secondary hedge if markets enter an elevated state of uncertainty.

We recently entered and exited a hedge position that returned 99% in 4 days through the use of Call Options. We bought Calls on .VIX with a $17 strike price Expiring on Aug. 20th @ $1.53 per contract.

Given the market recovery from the April lows and list of major events that aligned the week of Aug 1st, we calculated an extremely high level of volatility. The VIX experienced a 46% jump in the next 3 trading sessions moving from 15 to 21,90 allowing us to exit the call options at a sell price of $3.05 per contract. Equaling a 99.3% return.

We will continue to look for setups similar to the VIX call options above, as we foresee more market volatility going into the end of 2025. Paid subscribers will always be the first to know about our short-term high conviction setups.

Disclosure Statement for The Grosvenor Perception

Last Updated: 08/02/25

General Disclaimer

The Grosvenor Perception (“we,” “our,” or “the publication”) is a financial newsletter published by Michael Harbin. All content published in this newsletter, whether online, in email, or through any affiliated platforms, is intended for informational and educational purposes only. None of the information contained herein constitutes investment, financial, legal, or tax advice.

The views expressed in The Grosvenor Perception represent the personal opinions and analysis of the writers and contributors as of the date published and are subject to change at any time without notice. These opinions do not reflect the views of any affiliated institutions, employers, or entities.

No Investment Advice or Recommendations

The Grosvenor Perception is not a registered investment advisor, broker-dealer, or financial planner. We are not licensed under the U.S. Securities and Exchange Commission (SEC), Financial Industry Regulatory Authority (FINRA), or any other regulatory agency in any jurisdiction to provide personalized financial advice or investment recommendations.

Nothing published in this newsletter or on our website should be construed as a solicitation, offer, or recommendation to buy, sell, or hold any security or financial instrument. Subscribers and readers are solely responsible for their own investment decisions and should consult a licensed financial advisor, tax professional, or legal advisor before making any financial or investment decisions.

No Guarantee of Results or Performance

While we strive to provide accurate and up-to-date information, The Grosvenor Perception does not guarantee the accuracy, completeness, timeliness, or reliability of any information contained in our content. Financial markets are inherently uncertain and subject to numerous variables; past performance is not indicative of future results.

We disclaim all liability for any errors, omissions, or inaccuracies in the information presented. We make no representations or warranties—express or implied—regarding the effectiveness or profitability of any strategy, investment, or analysis discussed.

Forward-Looking Statements and Speculative Content

Some content in The Grosvenor Perception may contain forward-looking statements, projections, or speculative commentary, which are inherently uncertain and involve risks. These statements reflect our best judgment and interpretation at the time of publication but may not materialize as anticipated due to factors beyond our control.

Conflicts of Interest and Compensation

Writers and contributors to The Grosvenor Perception may have personal investments in securities or assets mentioned in the publication. Any such positions are not intended as recommendations and may be disclosed at the discretion of the author.

The newsletter may also contain sponsored content or affiliate links for which we may receive compensation. Any such material will be clearly marked in accordance with applicable FTC guidelines.

Copyright and Distribution

All content published in The Grosvenor Perception, including text, images, logos, and branding, is the intellectual property of Michael Harbin and is protected under applicable copyright laws. Unauthorized reproduction, redistribution, or public display of any portion of our content without written permission is strictly prohibited.

Jurisdiction and Legal Compliance

This publication is intended for a U.S.-based audience and is governed by the laws of the State of Florida, without regard to its conflict of laws principles. Access to the content of The Grosvenor Perception may not be legal for individuals in certain jurisdictions. It is the responsibility of the reader to ensure compliance with their local laws and regulations.

Contact Information

If you have questions about this disclosure or wish to contact the publisher of The Grosvenor Perception, please reach out to:

The Grosvenor Perception

admin@grosvenorperception.com

By reading this newsletter or accessing our content, you acknowledge that you have read, understood, and agreed to the terms outlined in this disclosure.

Member discussion